How I’m Navigating $100K in Home Improvement Quotes — And Why Pool Removal Still Makes The List

How I’m Navigating $100K in Home Improvement Quotes — And Why Pool Removal Still Makes The List

I asked for quotes. I got sticker shock.

Roof replacement — $25,000 to $35,000. New siding — $30,000 to $45,000. Windows — $20,000 to $30,000. New deck — $15,000 to $25,000. Pool removal — $15,000 to $20,000.

Add it all up and you’re staring at $100,000 to $155,000 in home improvement work. On a house you’re not planning to sell anytime soon. In an economy where uncertainty is the only certainty.

That number doesn’t just give you sticker shock. It paralyzes you.

So I did what any smart homeowner has to do — I stepped back, took a breath, and started thinking about this differently.

The Trap Most Homeowners Fall Into

The trap is thinking about home improvement as an all-or-nothing proposition. The house needs work. The quotes came in. Now you either do everything or you do nothing.

Neither is right.

The smart approach — the one that protects your cash flow, keeps your stress manageable, and still improves your home — is to piece meal these projects. Prioritize ruthlessly. Find the smart alternatives. Spread the work over 2 to 3 years instead of trying to do everything at once.

Here’s exactly how I’m thinking through it.

Project 1 — The Roof — Full Replacement vs Second Layer

My roof needs attention. That much is clear. The quotes for a full tear-off and replacement came in at $25,000 to $35,000.

But here’s what most homeowners don’t know — in Massachusetts you’re allowed to put a second layer of shingles directly over your existing roof without a full tear-off. Not every state allows this and it’s not always the right choice but when your existing roof is structurally sound with no leaks or rot it can be a legitimate and significantly cheaper option.

Second layer cost estimate — $12,000 to $18,000. Roughly half the price of a full replacement.

Is it the forever solution? No. Eventually the roof will need a full tear-off. But it buys you 10 to 15 more years and keeps $15,000 in your pocket today. In uncertain economic times that cash matters.

My other option — since we have no active leaks — is to repair the fascia boards and gutters where they’re failing, do a thorough inspection, and monitor for another year. Repair cost — $2,000 to $4,000. A fraction of either replacement option.

The lesson: Get the full replacement quote. Then ask what the alternatives are. There are almost always alternatives.

Project 2 — Siding — Full Replacement vs Repair and Paint

The siding quotes were brutal. $30,000 to $45,000 to replace wood siding with new vinyl or fiber cement.

But my siding is wood. And wood can be repaired, scraped, primed, and painted for a fraction of the replacement cost. Is it as good as new siding? No. Does it protect the house, dramatically improve curb appeal, and buy me another 8 to 12 years? Absolutely.

Repair damaged sections, scrape the peeling paint, prime everything properly, and apply two coats of quality exterior paint. Total cost — $8,000 to $14,000. Less than a third of full replacement.

Some contractors will tell you replacement is the only option. That’s because replacement is more profitable for them. Ask specifically about repair and paint as an alternative — you might be surprised what’s possible.

The lesson: Wood is repairable. Don’t let anyone tell you otherwise without getting a second opinion from someone who specializes in restoration rather than replacement.

The Mortgage Rate Trap — Why You Can’t Just Sell

Here’s the financial reality that nobody in the home improvement industry talks about — millions of American homeowners are effectively trapped in their homes by their mortgage rate.

If you bought or refinanced between 2020 and 2022 you probably have a mortgage rate between 2.5% and 4%. Today’s rates are 6.5% to 7.5%. The math on selling and buying elsewhere is brutal.

Let’s say your home is worth $500,000 and you have $200,000 in equity. Sounds great on paper. But if you sell and buy a comparable home at today’s rates your monthly payment could jump $1,500 to $2,500 per month. That equity evaporates in higher monthly payments within a few years.

So you stay. And you maintain and improve the home you’re in. Which is exactly the right decision — but it means you need to be smart about how you spend that improvement budget.

You can’t tap your equity to do everything at once and you can’t sell to access it without hurting yourself financially. You have to prioritize.

How To Prioritize Home Improvement Projects In 2026

Here’s the framework I’m using and I think it applies to most homeowners:

Priority 1 — Fix what protects the structure Roof leaks, foundation issues, water intrusion. These get worse and more expensive every year you wait. Fix them first even if it’s painful.

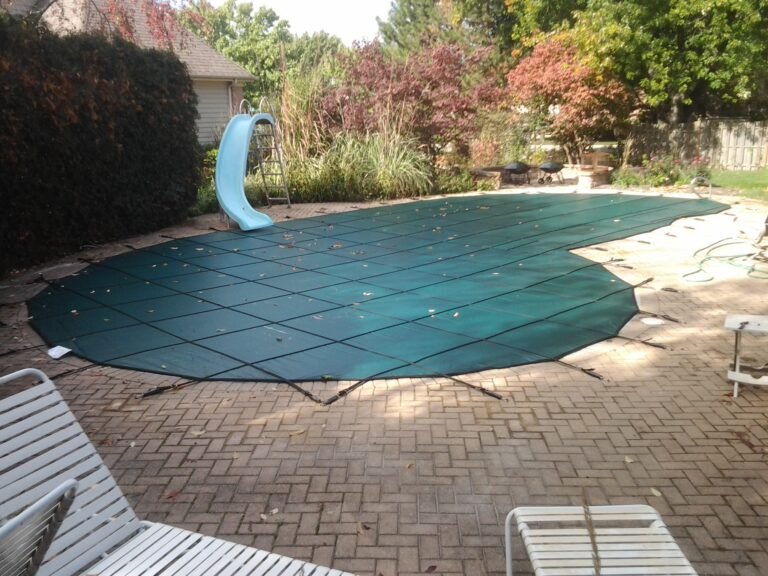

Priority 2 — Fix what’s actively costing you money This is where pool removal lands. Every year you don’t remove the pool costs you $3,000 to $8,000 in maintenance, chemicals, electricity, and heating. That’s real money leaving your account every single year. Removing the pool stops the bleeding permanently.

Priority 3 — Improve what has the best ROI Outdoor kitchens, updated bathrooms, kitchen improvements. Projects that add more value than they cost.

Priority 4 — Cosmetic improvements Paint, landscaping, flooring. Important but not urgent. These can wait.

Priority 5 — Everything else Windows, siding replacement, deck rebuilds. Important long term but manageable with smart alternatives in the short term.

Why Pool Removal Still Makes The List

I know what you’re thinking. If money is tight why is pool removal still on the priority list?

Because it pays for itself.

A pool removal costs $12,000 to $20,000. You’re currently spending $4,000 to $8,000 a year maintaining a pool you use 6 weeks. In 2 to 3 years the removal has paid for itself in maintenance savings alone. Every year after that is pure savings.

Compare that to new siding — costs $35,000, saves you nothing annually, just looks better. Or new windows — costs $20,000, saves a few hundred dollars a year in energy bills. The ROI on those projects measured in years is enormous.

Pool removal is one of the only major home improvement projects that actively saves you money every single year after it’s done. In uncertain economic times that annual savings is real, tangible, and valuable.

It’s not about having $20,000 to spend. It’s about understanding that spending $20,000 now saves you $5,000 a year forever. The math works. The timing just needs to be right.

The Plan Going Forward

Here’s where I’ve landed after weeks of thinking this through:

This year: Repair fascia and gutters — $2,000 to $4,000. Monitor the roof. Repair and paint the siding where needed — $8,000 to $12,000. Keep the pool covered. Save aggressively.

Next year: Pool removal — $15,000 to $20,000. Start planning the backyard transformation. Get contractor quotes over the winter.

Year after: Roof decision — second layer or full replacement depending on condition. Deck rebuild incorporating the new backyard vision.

Total spread over 3 years instead of $100,000 all at once. Manageable. Smart. Financially sound.

The Bottom Line

Home improvement in 2026 is about being strategic not impulsive. Get the quotes — all of them. Then ask about alternatives. Repair versus replace. Phase the work over multiple years. Protect your cash flow in uncertain times.

And when you’re evaluating which projects to do first — think about which ones save you money every single year after they’re done. Pool removal is near the top of that list for almost every homeowner who owns a pool they barely use.

I’m not removing my pool this year. But next year — with the house stabilized and the budget saved — it’s the first project on the list.

When you’re ready to remove your pool and start saving thousands every year — we can help you find verified contractors and get free quotes in your area.